The Thin Line Between Tax Avoidance and Tax Evasion in Nigeria: A Comprehensive Legal Analysis

Introduction

Taxation remains the primary source of revenue for any organized society, and Nigeria is no exception. The Nigerian government, through various statutory instruments, imposes taxes on individuals and corporate entities to fund public services, infrastructure, and governance. However, taxpayers often seek to minimize their tax liabilities, leading to the age-old debate between what constitutes legitimate tax avoidance and what amounts to criminal tax evasion.

While both concepts aim to reduce tax burdens, the legal consequences differ significantly. Tax avoidance, when conducted within the four corners of the law, is permissible and recognized by Nigerian courts. Tax evasion, on the other hand, is a criminal offense that attracts severe penalties. This article provides a comprehensive legal analysis of the distinction between tax avoidance and evasion under Nigerian law, examining the relevant legal framework, judicial pronouncements, permissible avoidance strategies, anti-avoidance measures, and enforcement mechanisms.

1. Conceptual Framework: Tax Avoidance vs. Tax Evasion

1.1 Definition of Tax Avoidance

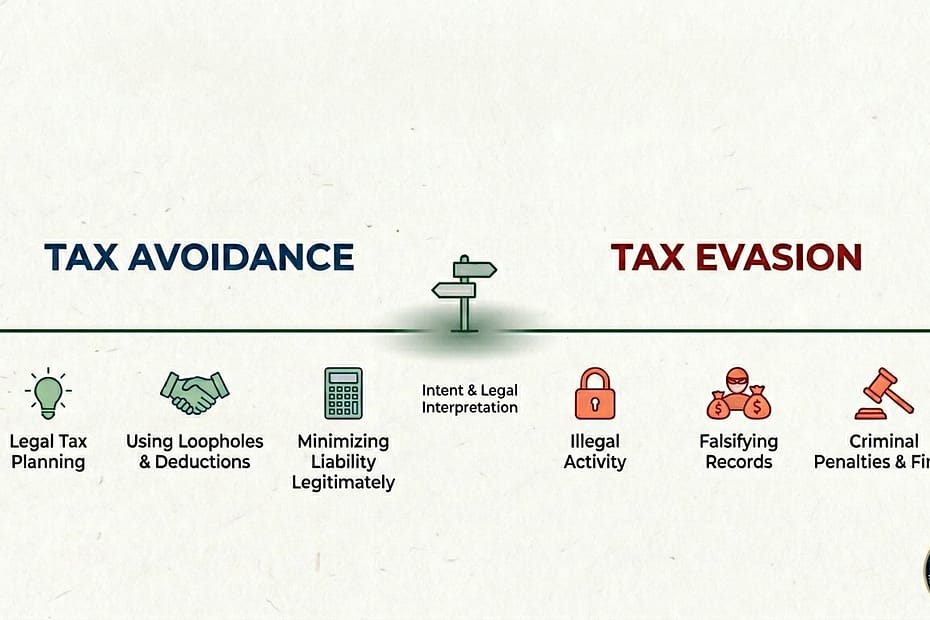

The 8th Edition of Black’s Law Dictionary defines tax avoidance as “the act of taking advantage of legally available tax-planning opportunities in order to minimize one’s tax liability”. Tax avoidance is a lawful means of altering a person’s taxable income to reduce the amount of tax owed, typically achieved by claiming tax deductions, tax credits, and positioning for tax incentives.

Nigerian law recognizes tax avoidance as a legitimate financial arrangement. As noted in legal literature, “tax avoidance is the use of tax laws to reduce tax payments”. Tax avoidance involves taking advantage of lawful provisions and incentives within the tax system to minimize tax exposure. Under the new Nigerian tax reforms, “avoidance is legitimate and encouraged, but aggressive or artificial schemes that lack commercial purpose may be reclassified as evasion”.

1.2 Definition of Tax Evasion

Tax evasion is the illegal evasion of taxes by taxpayers through fraudulent means. It is “an illegal act of intentionally reducing accrual taxes or completely skipping the payment of such taxes by under reporting income, overstating expenditures, deductions or exemptions”.

Tax evasion has also been interpreted to mean “an illegal practice where a person, organization, or corporation deliberately evades paying their authentic tax liability by deliberately not declaring all taxable income”. Common instances of tax evasion include:

- False declaration of one’s financial status

- Failure to render tax returns as appropriate

- Manipulation of accounts with intent to hide actual taxable profits

In Independent Television/Radio v. E.S.B.I.R. [2015] 12 NWLR (Pt. 1474) 442, where the taxpayer failed to render tax returns to the relevant tax authority, the court held that this was “a despicable way for any taxpayer to act and it is seriously detrimental to the development of any nation”.

2. The Legal Basis for Tax Avoidance in Nigeria

2.1 Constitutional Foundation

The duty to pay taxes in Nigeria is constitutionally backed by Section 24(f) of the 1999 Constitution of the Federal Republic of Nigeria (as amended), which provides that “it shall be the duty of every citizen to declare his income honestly to appropriate and lawful agencies and pay his tax promptly”.

In Independent Television/Radio v. E.S.B.I.R. [2015] 12 NWLR (Pt. 1474) 442, the court reiterated the constitutional duty of a citizen to pay tax, stating that “failure of the citizen to pay tax shall strip him of the protection afforded by section 44(1) of the Constitution”.

2.2 Judicial Recognition of Tax Avoidance

Nigerian courts have consistently recognized the right of taxpayers to arrange their affairs to minimize tax liability. In G. M. Akinsete Syndicate v. Senior Inspector of Taxes, Akure, the Supreme Court recognized that a person may use lawful means to avoid tax; what he may not do is to try to evade tax.

This judicial attitude traces back to English jurisprudence. In Ayrshire Pullman Motor Services v. IRC, Lord Clyde famously stated:

“The Inland Revenue is not slow – and quite rightly – to take every advantage, which is open to it under the taxing statutes, for the purpose of depleting the taxpayer’s pocket. And the taxpayer is, in like manner, entitled to be astute to prevent, so far as he honestly can, the depletion of his means by the Inland Revenue.”

Similarly, in Duke of Westminster v. CIR, Lord Tomlin made his famous pronouncement that “every man is entitled, if he can, to order his affairs so that the tax attaching under the appropriate Acts is less than it otherwise would be”.

In the Nigerian context, the Federal High Court, Lagos Division, in JGC Corporation v. FIRS (2016) 22 TLRN 37, upheld the rights of taxpayers to embark on tax planning exercises and structure their business transactions to reduce or eliminate their liability to tax.

2.3 Mobil Oil (Nig.) Ltd. v. FBIR

In Mobil Oil (Nig.) Ltd. v. FBIR (1922–2014) All NTC 203, the court provided a practical definition of tax evasion, noting that it generally refers to situations where taxable persons manipulate their accounts with intent to hide their actual taxable profits and evade the tax they ought to have paid.

3. Lawful Tax Avoidance Strategies

Nigerian tax laws provide several legal avenues for taxpayers to reduce their tax liabilities. Below are the primary strategies recognized under Nigerian law.

3.1 Reinvestment of Proceeds from Asset Sales (Capital Gains Tax Deferral)

Under the Capital Gains Tax Act and the Nigeria Tax Act 2025, profits from the disposal of assets attract a 10% capital gains tax. However, where the proceeds are reinvested in assets of the same class, payment of the tax can be deferred.

Practical Example: If a company sells a generator and uses the proceeds to acquire another generator within 12 months before or after the sale, the capital gains tax becomes deferred for as long as the new asset remains in use. This relief does not apply if the proceeds are used to purchase assets of a different class, such as vehicles.

Section 34(1)(a)(iii) of the Nigeria Tax Act 2025 explains that gains from selling shares in Nigerian companies are exempt from capital gains tax if proceeds are reinvested within the same year. The law also exempts smaller transactions, including disposals under N150 million with gains below N10 million.

3.2 Offset Input VAT Against Output VAT

Businesses registered for Value Added Tax (VAT) are allowed to deduct input VAT (VAT paid on purchases) from output VAT (VAT charged on sales).

Practical Example: If a business pays N500,000 VAT on raw materials and later charges N750,000 VAT on finished goods sold, only the net N250,000 should be remitted to the government. Many businesses fail to make this deduction, resulting in unnecessary overpayment.

The Finance Act 2019 introduced a VAT anti-avoidance rule empowering the tax authorities to make necessary adjustments to counteract the effect of any artificial or fictitious transaction.

3.3 Registration as an NGO or Limited by Guarantee

Organizations registered as Limited by Guarantee, such as charities, religious institutions, and NGOs, are generally exempt from company income tax. While such entities are prohibited from sharing profits as dividends, they enjoy tax relief on operational income.

However, the tax exemption is conditional and not absolute. Under FIRS Information Circular No. 01/2025, NGOs have tax obligations including registration with FIRS for tax purposes and filing of annual tax returns. Income from investments, such as dividends, still attracts withholding tax. Businesses focused on social impact or charity may benefit from this structure.

3.4 Capital Allowances on Business Assets

Capital allowances serve as tax relief for the wear and tear of business assets such as machinery and equipment. To benefit, companies must obtain a Certificate of Acceptance from the Ministry of Trade and a Capital Allowance Certificate from the Ministry of Industry. These certificates allow companies to deduct capital allowances from taxable profits, significantly reducing income tax obligations.

3.5 Withholding Tax Credit Notes

Withholding Tax (WHT) deducted on contracts for supplies and services is not a final tax but an advance payment of income tax. Businesses must ensure they collect WHT credit notes from clients who deduct tax from their invoices. These credits can then be offset against total tax liabilities, preventing double taxation and excessive payments.

4. Aggressive Tax Avoidance and Anti-Avoidance Measures

While tax avoidance is legal, aggressive tax avoidance schemes that lack commercial substance are problematic. As noted by Samson Olubode, a chief finance officer, “though tax avoidance is legal, aggressive tax avoidance schemes are problematic”.

4.1 General Anti-Avoidance Rules (GAAR)

General anti-avoidance rules (GAARs) were included in Nigeria’s income tax laws as a means of curbing tax avoidance. Tax authorities have relied on GAARs to assess and regulate the pricing of inter-group transactions where such transactions appeared to be artificial or sham arrangements.

The Nigeria Finance Act 2022 introduced a comprehensive GAAR to counteract arrangements or transactions that have the main purpose of obtaining a tax advantage. GAAR empowers tax authorities to disregard or recharacterize such transactions for tax purposes.

Key provisions under the Finance Act 2022 include:

- Controlled Foreign Company (CFC) Rules: Income of a foreign company controlled by Nigerian residents may be attributed to Nigerian shareholders and subject to taxation in Nigeria.

- Thin Capitalization Rules: These rules prevent excessive interest deductions by limiting the amount of interest expenses that can be claimed on loans from related parties.

- Transfer Pricing Regulations: The Act enhances transfer pricing regulations, requiring related-party transactions to be conducted at arm’s length. Tax authorities are empowered to make adjustments to transactions that do not meet arm’s length standards.

4.2 Section 47 of the Nigeria Tax Administration Act 2025

Section 47 of the Nigeria Tax Administration Act 2025 provides a codified definition of “prohibited tax avoidance arrangement.” The section states that the relevant tax authority may counteract a prohibited tax avoidance arrangement by way of adjustments, disregarding, or recharacterizing the arrangement through an assessment, unless the taxable person proves that granting the benefit would be in accordance with the object and purpose of the relevant provisions.

A prohibited tax avoidance arrangement exists where, having regard to the facts and circumstances, it is reasonable to conclude that:

- The main purpose of the arrangement was to obtain a tax benefit or advantage;

- Obtaining the tax advantage is contrary to the object and purpose of the provisions of the Act or any other tax law;

- It results, directly or indirectly, in the misuse or abuse of the provisions of the Act or any other tax law; or

- It lacks commercial substance or coherence in whole or in part.

4.3 Transfer Pricing Regulations

Transfer pricing deals with the setting of prices for transactions between related parties, with the goal of preventing the mispricing of such transactions through underpricing or overpricing by related parties. TP regulation in Nigeria is based on the provisions in the various taxing statutes, commonly referred to as GAAR.

In August 2012, the Federal Inland Revenue Service (FIRS) published Nigeria’s first transfer pricing regulations, which were replaced by the Income Tax (Transfer Pricing) Regulations 2018. The 2018 Regulations include rules on intra-group services, pricing of intangibles, pricing of commodities, exports and imports, and transfer pricing documentation processes.

5. Legal Consequences of Tax Evasion

5.1 Statutory Provisions

Section 40 of the Federal Inland Revenue Service Act (FIRSEA) 2007 makes tax evasion illegal in Nigeria. Tax evaders face criminal charges and are liable to pay the withheld tax and a 10% penalty per annum. Any infraction attracts a fine or an imprisonment term of three years or both.

Additionally, obstructing or assaulting any authorized tax officer in the exercise of their responsibilities is a criminal offense under Section 41 of the FIRSEA Act.

5.2 Non-filing of Tax Returns

Under the Companies Income Tax Act (CITA), failure to remit tax after 30 days constitutes an offense, with penalties starting at N25,000 for the first default month and N5,000 for subsequent months.

5.3 EFCC’s Jurisdiction to Prosecute Tax Evasion

A significant development occurred when the Court of Appeal held that the Economic and Financial Crimes Commission (EFCC) has the legal power to investigate and prosecute tax evasion. This judgment effectively ended the argument that only the FIRS could handle tax matters. As one commentator noted, “Tax evasion is no longer ‘just a tax office issue.’ The Court of Appeal has made it clear”.

5.4 Case Law: Court Orders Firm to Remit N1.4bn Unpaid Taxes

In a recent judgment, Justice Champion Umukoro of Delta Revenue Court sitting in Warri ruled in favor of the Delta State Board of Internal Revenue (DSBIRS) in a tax evasion case against a labor-providing firm to Chevron Nigeria Limited. The court ordered the firm to remit N1.4 billion unpaid taxes.

6. The 2025 Tax Reforms: Key Developments

6.1 Nigeria Tax Act 2025 and Nigeria Tax Administration Act 2025

The new tax laws, anchored by the Nigeria Tax Administration Act 2025, form part of the Federal Government’s broader fiscal reform agenda to boost revenue mobilization, improve transparency, and reduce reliance on borrowing.

Key features include:

- Clearer rules on double taxation relief

- Digital economy taxation

- Virtual asset service provider regulations

- Enhanced record-keeping and dispute resolution

- Incentives for research, development, and export-oriented businesses

6.2 Substance-over-Form Approach

Under the new framework, tax authorities are allowed to “disregard any disposition or transaction” considered artificial and make adjustments to counteract any reduction in tax liability. The provision signals a shift in how tax compliance will be assessed, moving beyond the legal form of transactions to focus on their underlying economic reality.

Multinational companies that use artificial deductions or complex structures to reduce their tax burden below the minimum effective tax rate of 15% are expected to come under increased scrutiny.

6.3 FIRS Halts Issuance of Tax Exemption Certificates

In July 2025, the FIRS officially halted the issuance of tax exemption certificates to all categories of taxpayers, including pioneer status companies, NGOs, and businesses operating within Nigeria’s free trade zones. The Executive Chairman of FIRS, Zacch Adedeji, noted that Nigeria loses billions annually due to aggressive tax avoidance by multinational corporations.

6.4 Nigeria Revenue Service (NRS) Replaces FIRS

The Nigeria Revenue Service (NRS) now replaces the FIRS as the central tax authority. Enforcement tools now include powers to trace, freeze, or seize assets linked to evasion, a Central Taxpayer Database for nationwide monitoring, and international collaboration on cross-border tax information exchange.

7. Practical Examples: Distinguishing Legitimate Avoidance from Evasion

7.1 Legitimate Tax Avoidance

| Strategy | Legal Basis | Example |

|---|---|---|

| CGT Deferral | CGT Act, Nigeria Tax Act 2025 s.34(1)(a)(iii) | Company sells factory equipment for N50M, reinvests proceeds in new equipment within 12 months – CGT deferred |

| Input VAT Offset | VAT Act | Business pays N500k input VAT, charges N750k output VAT – only N250k remitted |

| NGO Registration | CITA (as amended) | Charity organization exempt from CIT on operational income |

| Capital Allowances | CITA | Manufacturing company claims 25% annual allowance on N100M machinery – reduces taxable profit by N25M |

7.2 Illegal Tax Evasion

| Act | Legal Consequence | Example |

|---|---|---|

| Underreporting Income | Criminal prosecution, 10% penalty p.a., imprisonment up to 3 years | Business declares N10M income when actual income is N50M |

| Failure to File Returns | N25,000 first month, N5,000 subsequent months | Company operates for 5 years without filing any tax returns |

| Artificial Transactions | GAAR invocation, transaction disregarded | Creating sham intra-group loans to shift profits offshore |

| Offshore Profit Shifting | CFC Rules, transfer pricing adjustments | Nigerian company pays inflated royalties to related Cayman Islands entity |

8. The Economic Impact of Tax Evasion

According to available records, Nigeria is home to over 440,000 registered companies; however, only about 120,000 of these companies are tax-compliant. This means that approximately 320,000 companies are not paying their fair share of taxes, resulting in substantial loss of revenue for the nation.

The FIRS Executive Chairman has repeatedly highlighted that Nigeria loses billions of naira annually due to aggressive tax avoidance, which undermines governance, erodes trust, and worsens inequality.

9. Conclusion and Recommendations

The distinction between lawful tax avoidance and criminal tax evasion is clear under Nigerian law: avoidance involves using legal provisions to minimize tax liability, while evasion involves fraudulent concealment or misrepresentation to avoid paying taxes lawfully due.

Nigerian courts have consistently upheld the right of taxpayers to arrange their affairs to minimize tax liability, as seen in Akinsete Syndicate v. Senior Inspector of Taxes, JGC Corporation v. FIRS, and the adoption of the Duke of Westminster principle. However, the law has evolved significantly with the introduction of GAAR, transfer pricing regulations, and the Nigeria Tax Administration Act 2025.

Key Recommendations for Taxpayers:

- Engage qualified tax professionals to ensure compliance

- Document all transactions with clear commercial substance

- Obtain advance tax rulings for complex structures

- Regularly review holding structures and related-party transactions

- Maintain proper transfer pricing documentation

- File all tax returns promptly and accurately

- Utilize legitimate tax incentives and reliefs as provided by law

As the legal maxim goes: “Every man is entitled to order his affairs so that the tax attaching under the appropriate Acts is less than it otherwise would be.” However, this right must be exercised honestly, transparently, and within the bounds of the law.

Disclaimer: This article is for informational purposes only and does not constitute legal advice. Readers should consult qualified legal practitioners for advice specific to their circumstances.

References & Citations

[2015] 12 NWLR (Pt. 1474) 442

Supreme Court of Nigeria decision recognizing lawful tax avoidance.

House of Lords landmark case establishing the right of taxpayers to order their affairs to minimize tax.

(2016) 22 TLRN 37

(1922–2014) All NTC 203

Federal Republic of Nigeria official gazette and statutory reform instrument.

Section 40 and 41 of the FIRSEA 2007 establishing tax evasion penalties.